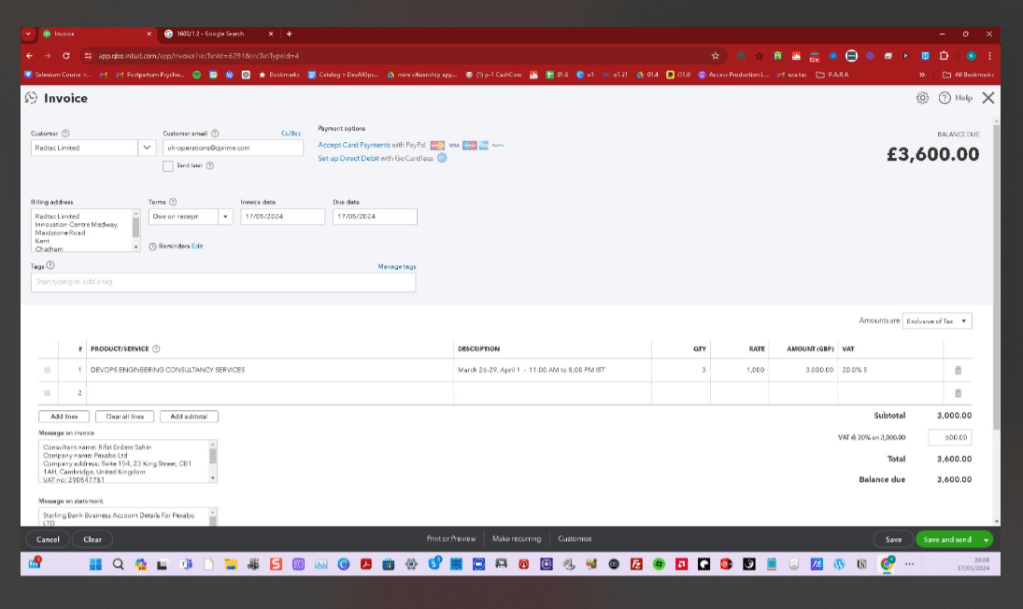

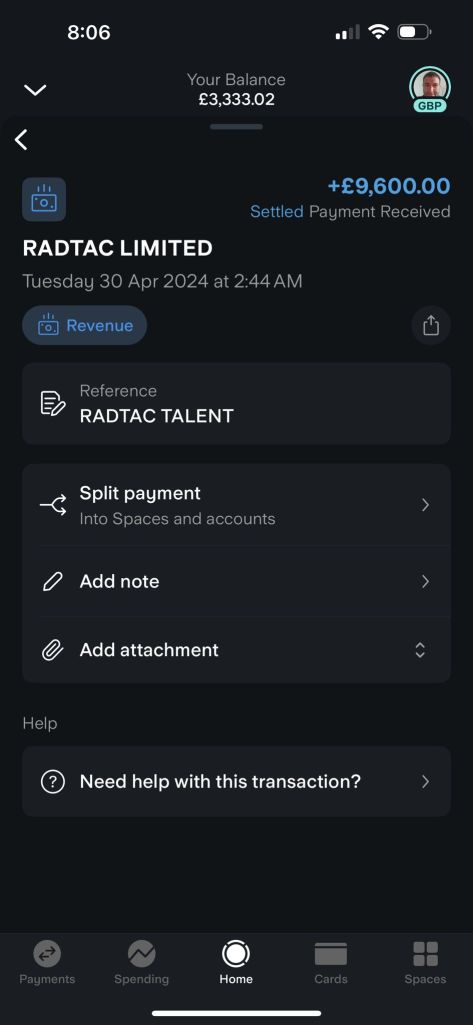

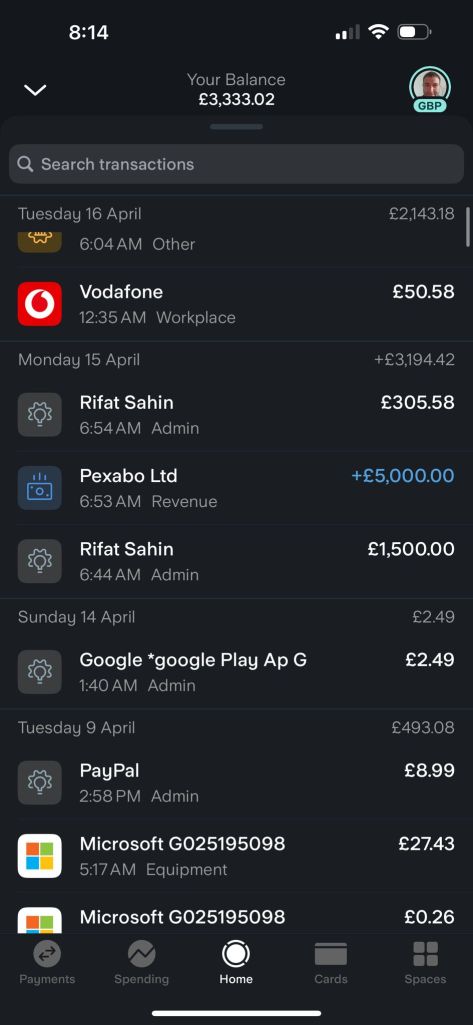

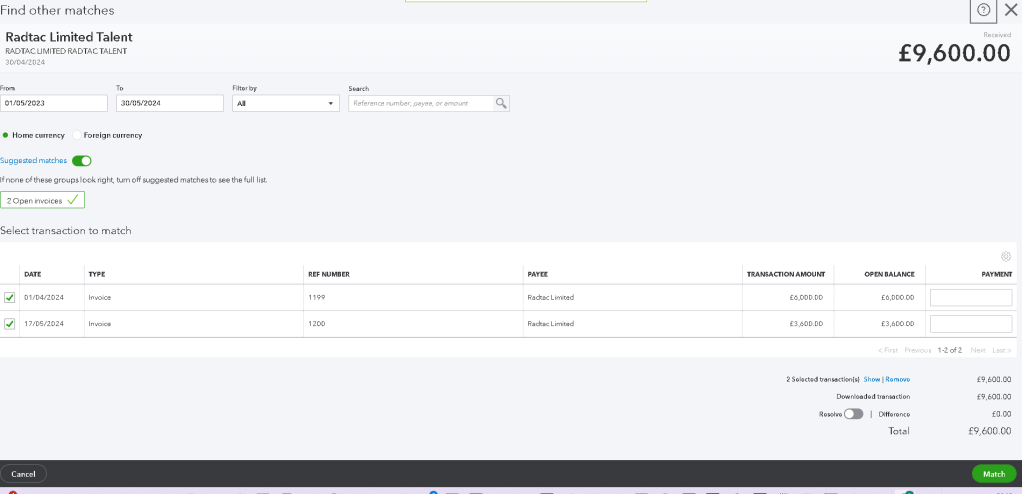

Line up the numbers in Quickbooks using GPT 4.0 this time

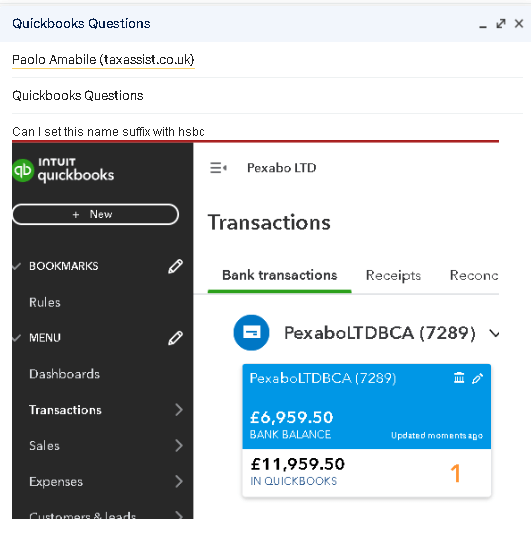

diff from 6000

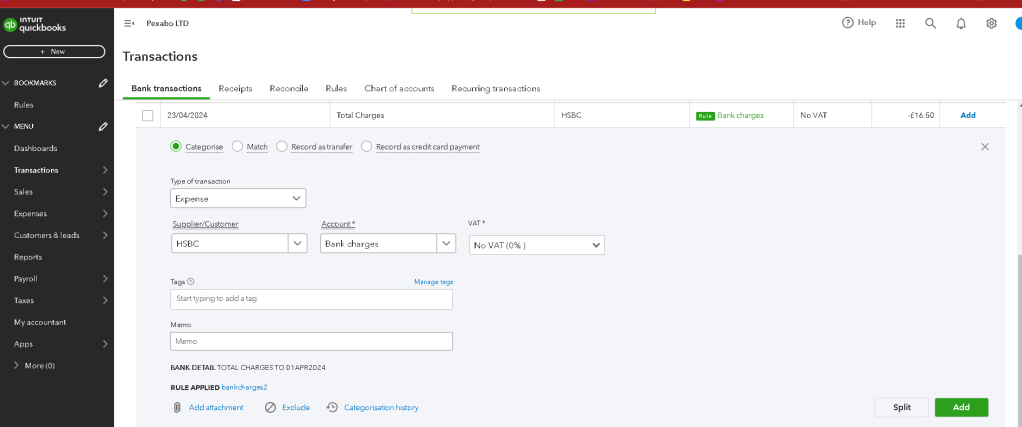

In the UK, most bank charges are generally exempt from Value Added Tax (VAT). The exemption covers many standard banking services such as account maintenance fees, transaction charges, and loan arrangement fees. However, there are some exceptions where VAT may be applicable:

-

Advisory Services: If a bank provides advisory services, such as investment advice or consultancy, these services might be subject to VAT.

-

Non-standard Services: Some specialized banking services that are not directly related to financial transactions could be subject to VAT. For example, charges for safe deposit box rentals may attract VAT.

-

Ancillary Services: Fees for services ancillary to financial transactions, like certain types of administrative fees, might also be subject to VAT.

For businesses, it's important to review the specific nature of the bank charges to determine if VAT is applicable. Consulting with a tax advisor or the bank itself can provide clarity on whether any specific charges will include VAT.

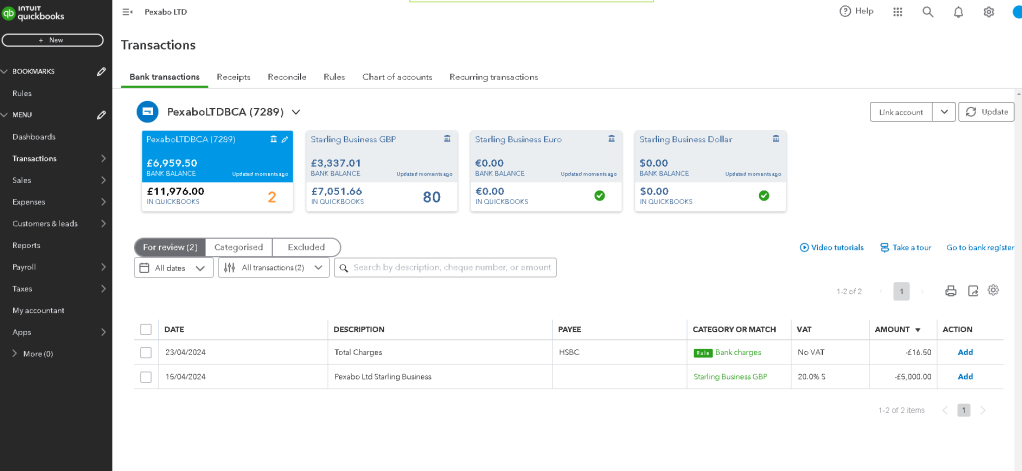

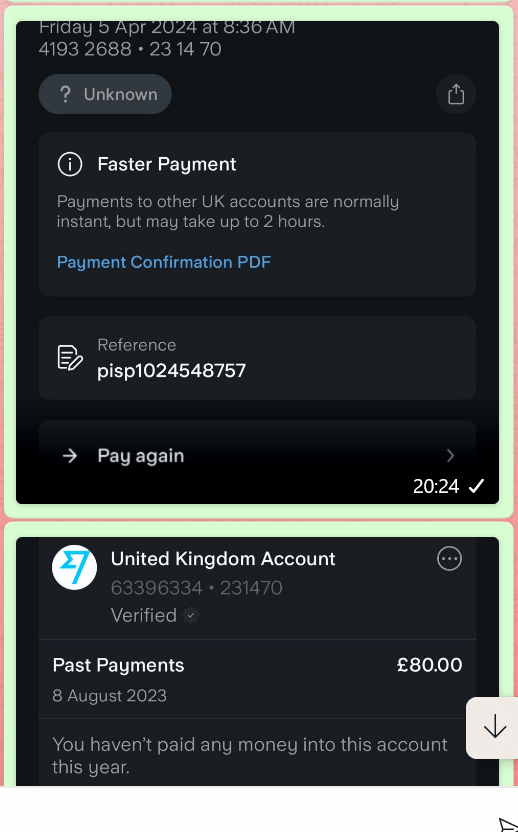

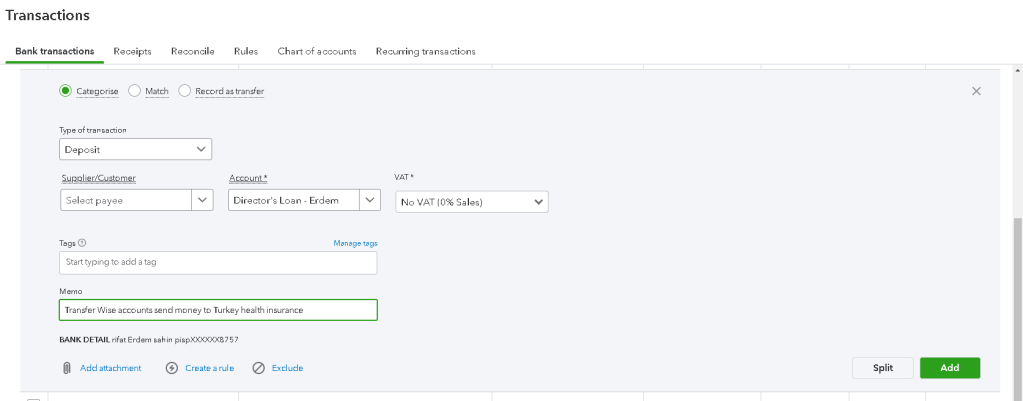

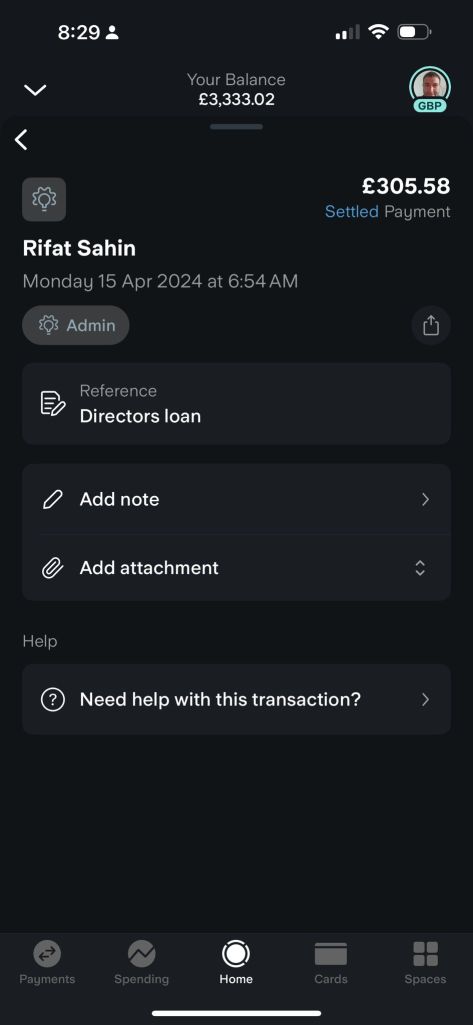

this is a transfer

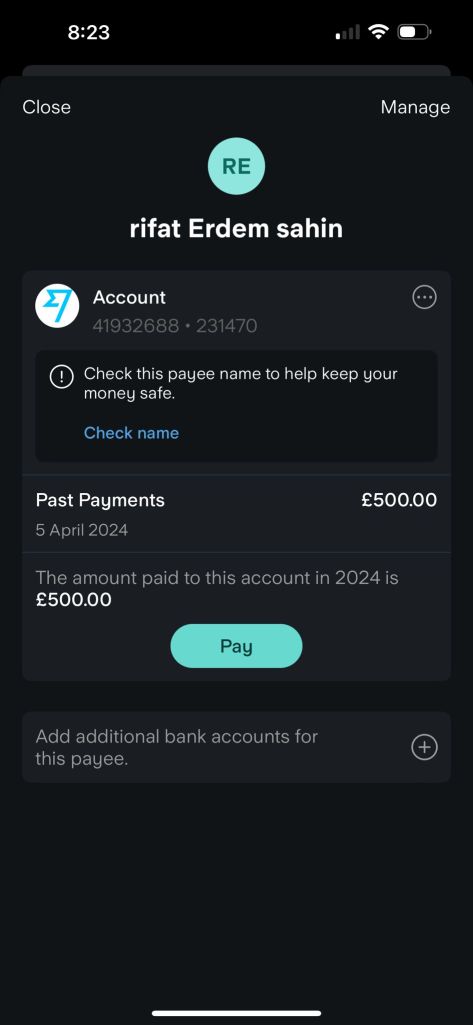

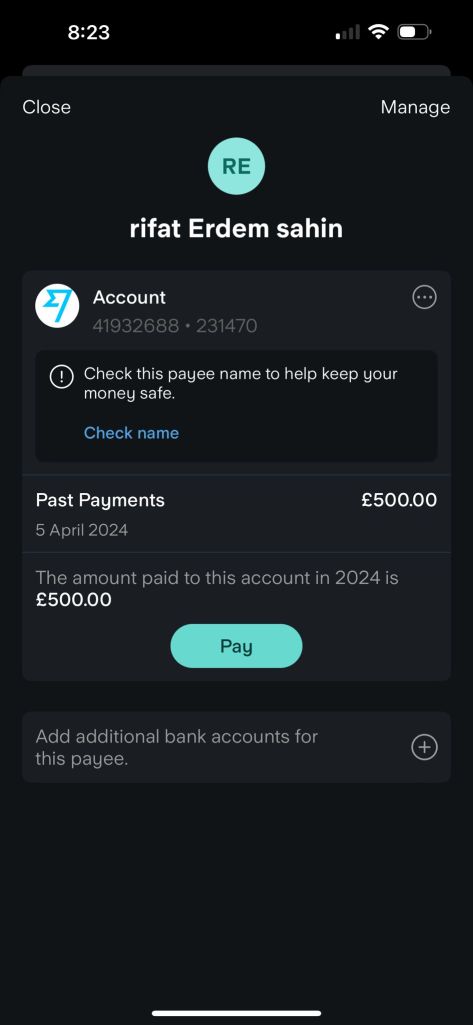

Ask the bank account name update for visibility

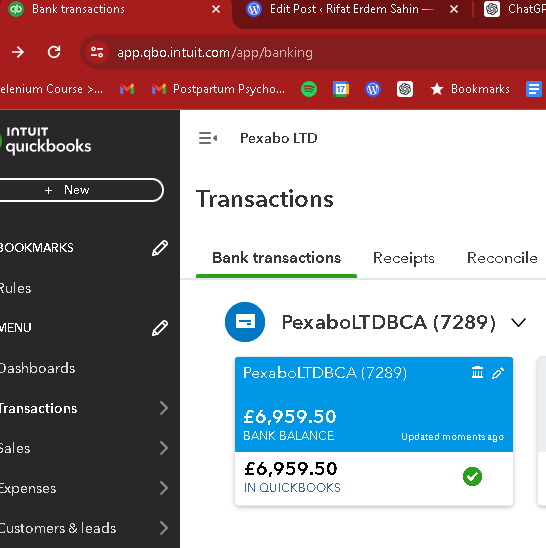

Once numbers are mathced it means i did it correctly ?

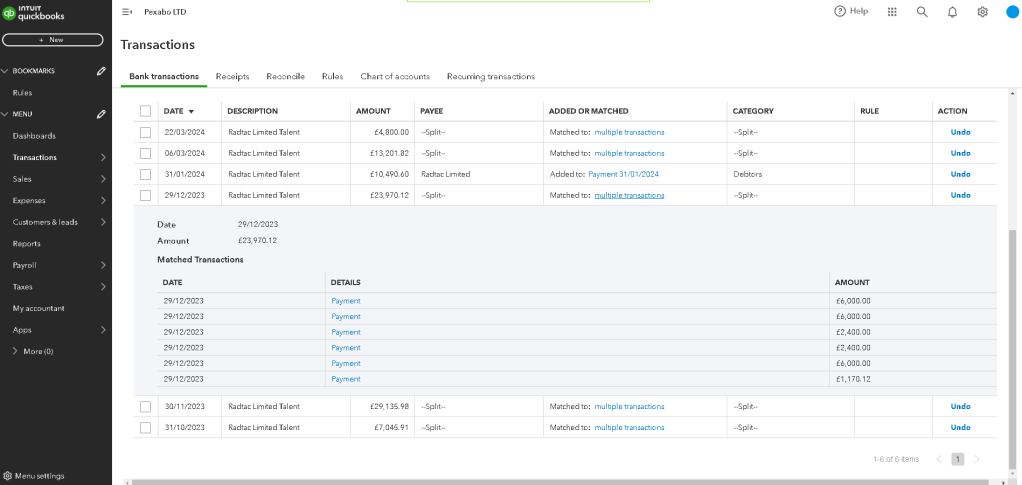

I need to learn how to match multiple

Lets see if the match system works

Director Loan

Wise accounts

description mention it is easier

DEfault director loan at the end of the year it is divident if taken out a lot

The tax treatment of taking money as dividends versus a director's loan in the UK differs significantly. Here's a breakdown of the differences:

Dividends

-

Tax Treatment for the Company:

-

Dividends are paid out of the company’s profits after Corporation Tax has been applied.

-

Dividends do not reduce the company’s taxable profits.

-

Tax Treatment for the Individual:

-

Dividend Allowance: As of the 2023/24 tax year, there is a £1,000 tax-free dividend allowance.

-

Tax Rates on Dividends:

Basic Rate: 8.75%

-

Higher Rate: 33.75%

-

Additional Rate: 39.35%

-

Dividends are not subject to National Insurance Contributions (NICs).

Director’s Loan

-

Tax Treatment for the Company:

-

If a director takes out a loan from the company, it must be repaid within nine months and one day after the end of the accounting period to avoid extra tax charges.

-

If not repaid on time, the company must pay a 33.75% tax (known as Section 455 tax) on the outstanding loan balance.

-

If the loan is eventually repaid, the company can reclaim the Section 455 tax, but this can take time.

-

Tax Treatment for the Individual:

-

If the loan exceeds £10,000 at any point during the tax year, it is treated as a beneficial loan and subject to Benefit in Kind (BIK) rules.

-

The individual must pay tax on the BIK at their marginal rate, and the company must pay Class 1A NICs on the BIK.

-

If the loan is written off, it is treated as income and taxed as a dividend, which could also mean NICs are due.

Summary

-

Dividends:

-

Pros: Lower tax rates for individuals, no NICs.

-

Cons: Paid out of post-tax profits, impacts distributable reserves.

-

Director’s Loan:

-

Pros: Immediate access to funds, potential tax deferral.

-

Cons: Repayment requirements to avoid additional tax charges, potential BIK implications, and complex tax handling if not repaid.

The choice between taking money as dividends or a director’s loan depends on several factors, including the company’s financial position, the director’s personal tax situation, and cash flow needs. Consulting with a tax advisor can provide tailored advice based on specific circumstances.

Imported from rifaterdemsahin.com · 2024